Contemplating Pensions

RIGHEIMER'S THEME SONG

Much has been said and written about Costa Mesa employee pensions over the past couple years. The "dire" condition of our unfunded pension liability has been the cornerstone of much of what Mayor Jovial Jim Righeimer has tried to do since he took office two years ago. If you listened to him you'd think our world as we know it was coming to an end - that our streets would turn to cobblestones, our playing fields into gravel pits and our parks into weed-filled pastures unless we "solved" the pension problem. To hear him talk you'd think our fire fighting force will be reduced to horse-drawn hand pumpers and our police service would resemble - wait for it - Mayberry.

Much has been said and written about Costa Mesa employee pensions over the past couple years. The "dire" condition of our unfunded pension liability has been the cornerstone of much of what Mayor Jovial Jim Righeimer has tried to do since he took office two years ago. If you listened to him you'd think our world as we know it was coming to an end - that our streets would turn to cobblestones, our playing fields into gravel pits and our parks into weed-filled pastures unless we "solved" the pension problem. To hear him talk you'd think our fire fighting force will be reduced to horse-drawn hand pumpers and our police service would resemble - wait for it - Mayberry.

NUMBERS, NUMBERS, NUMBERS

Over the past few years the city has provided us with the testimony of "experts" in the field to attempt to assist Finance and Information Technology Director Bobby Young in making the almost incomprehensible mountain of data understandable. We've heard numbers thrown around in the hundreds of millions of dollars. At one point we were told by consultant John Bartel that our then-current unfunded liability of around $200 million payable over 30 years would turn into an immediate due-upon-demand bill of over $350 million if we opted out of CalPERS.

Over the past few years the city has provided us with the testimony of "experts" in the field to attempt to assist Finance and Information Technology Director Bobby Young in making the almost incomprehensible mountain of data understandable. We've heard numbers thrown around in the hundreds of millions of dollars. At one point we were told by consultant John Bartel that our then-current unfunded liability of around $200 million payable over 30 years would turn into an immediate due-upon-demand bill of over $350 million if we opted out of CalPERS.

MONEY DOWN THE DRAIN?

Last week Stanford University professor Joe Nation - a former Democratic politician who got a real job after failing to be re-elected - told us in clear, unambiguous terms about our pension situation. At the end of his presentation and the short one that followed by Young, Righeimer made a short speech in which he told us clearly that he was not interested in sending additional money to CalPERS to pay down the unfunded liability. I quoted him thus:

Last week Stanford University professor Joe Nation - a former Democratic politician who got a real job after failing to be re-elected - told us in clear, unambiguous terms about our pension situation. At the end of his presentation and the short one that followed by Young, Righeimer made a short speech in which he told us clearly that he was not interested in sending additional money to CalPERS to pay down the unfunded liability. I quoted him thus:

"There's no way this is going to get paid off. It can't be paid off. That's another 15-18 million dollars a year. There's going to have to be some movement from the state legislature and PERS to go ahead and change benefits going forward for existing employees. That will not happen in the State of California until it crashes." He went on to say, "The situation is 'Where is Costa Mesa going to be when that happens?' and I, for one, am not interested in giving additional payments to PERS. I don't mind putting it aside somewhere else, but I can't imagine sending them an additional 10-15 million dollars a year when it can just disappear tomorrow and we'll be tossed into the same category with everyone else."

CALPERS DOOMED?

I guess his presumption is that CalPERS is doomed to failure because the state legislature and the CalPERS board are dominated by those nasty Democrats - liberals who will simply let it self-destruct before doing anything - and he didn't want to send any additional monies into that black hole. I don't know, maybe he's correct, but it's hard for me to imagine any responsible group letting that happen without drastic action - even a bunch of "nasty Democrats".

I guess his presumption is that CalPERS is doomed to failure because the state legislature and the CalPERS board are dominated by those nasty Democrats - liberals who will simply let it self-destruct before doing anything - and he didn't want to send any additional monies into that black hole. I don't know, maybe he's correct, but it's hard for me to imagine any responsible group letting that happen without drastic action - even a bunch of "nasty Democrats".

JUST RHETORIC?

Some might interpret Righeimer's comments as more political rhetoric. They might be right. After all, if a guy's going to run for higher office he needs a plank in his campaign platform that is broader than little old Costa Mesa. His pal and OCGOP honcho Scott Baugh has stated that our city is "Ground Zero" for state-wide pension reform.

Some might interpret Righeimer's comments as more political rhetoric. They might be right. After all, if a guy's going to run for higher office he needs a plank in his campaign platform that is broader than little old Costa Mesa. His pal and OCGOP honcho Scott Baugh has stated that our city is "Ground Zero" for state-wide pension reform.

A GREAT SITE

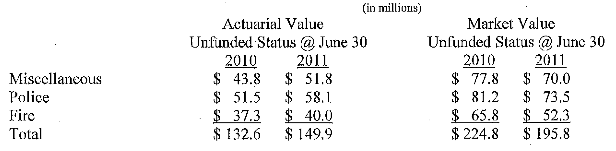

The pension numbers make my head hurt, but Communication Director Bill Lobell and Young have put together a site where you can find every answer to every question you might have about Costa Mesa pensions, HERE. It also includes a link, HERE, to a letter Young sent to the council in December that capsulizes much of that good information. The chart below is taken from that letter. (click on image to enlarge)

The pension numbers make my head hurt, but Communication Director Bill Lobell and Young have put together a site where you can find every answer to every question you might have about Costa Mesa pensions, HERE. It also includes a link, HERE, to a letter Young sent to the council in December that capsulizes much of that good information. The chart below is taken from that letter. (click on image to enlarge)

CLICK AWAY

CLICK AWAY

So, if you REALLY want to learn about our pension situation, visit the city page and just click away on the links provided. Have a bottle of Tylenol handy. In the meantime, we'll just have to see what Righeimer has up his sleeve on this subject. Don't blink...

So, if you REALLY want to learn about our pension situation, visit the city page and just click away on the links provided. Have a bottle of Tylenol handy. In the meantime, we'll just have to see what Righeimer has up his sleeve on this subject. Don't blink...

Much has been said and written about Costa Mesa employee pensions over the past couple years. The "dire" condition of our unfunded pension liability has been the cornerstone of much of what Mayor Jovial Jim Righeimer has tried to do since he took office two years ago. If you listened to him you'd think our world as we know it was coming to an end - that our streets would turn to cobblestones, our playing fields into gravel pits and our parks into weed-filled pastures unless we "solved" the pension problem. To hear him talk you'd think our fire fighting force will be reduced to horse-drawn hand pumpers and our police service would resemble - wait for it - Mayberry.

Much has been said and written about Costa Mesa employee pensions over the past couple years. The "dire" condition of our unfunded pension liability has been the cornerstone of much of what Mayor Jovial Jim Righeimer has tried to do since he took office two years ago. If you listened to him you'd think our world as we know it was coming to an end - that our streets would turn to cobblestones, our playing fields into gravel pits and our parks into weed-filled pastures unless we "solved" the pension problem. To hear him talk you'd think our fire fighting force will be reduced to horse-drawn hand pumpers and our police service would resemble - wait for it - Mayberry.NUMBERS, NUMBERS, NUMBERS

Over the past few years the city has provided us with the testimony of "experts" in the field to attempt to assist Finance and Information Technology Director Bobby Young in making the almost incomprehensible mountain of data understandable. We've heard numbers thrown around in the hundreds of millions of dollars. At one point we were told by consultant John Bartel that our then-current unfunded liability of around $200 million payable over 30 years would turn into an immediate due-upon-demand bill of over $350 million if we opted out of CalPERS.MONEY DOWN THE DRAIN?

Last week Stanford University professor Joe Nation - a former Democratic politician who got a real job after failing to be re-elected - told us in clear, unambiguous terms about our pension situation. At the end of his presentation and the short one that followed by Young, Righeimer made a short speech in which he told us clearly that he was not interested in sending additional money to CalPERS to pay down the unfunded liability. I quoted him thus:"There's no way this is going to get paid off. It can't be paid off. That's another 15-18 million dollars a year. There's going to have to be some movement from the state legislature and PERS to go ahead and change benefits going forward for existing employees. That will not happen in the State of California until it crashes." He went on to say, "The situation is 'Where is Costa Mesa going to be when that happens?' and I, for one, am not interested in giving additional payments to PERS. I don't mind putting it aside somewhere else, but I can't imagine sending them an additional 10-15 million dollars a year when it can just disappear tomorrow and we'll be tossed into the same category with everyone else."

CALPERS DOOMED?

I guess his presumption is that CalPERS is doomed to failure because the state legislature and the CalPERS board are dominated by those nasty Democrats - liberals who will simply let it self-destruct before doing anything - and he didn't want to send any additional monies into that black hole. I don't know, maybe he's correct, but it's hard for me to imagine any responsible group letting that happen without drastic action - even a bunch of "nasty Democrats".JUST RHETORIC?

Some might interpret Righeimer's comments as more political rhetoric. They might be right. After all, if a guy's going to run for higher office he needs a plank in his campaign platform that is broader than little old Costa Mesa. His pal and OCGOP honcho Scott Baugh has stated that our city is "Ground Zero" for state-wide pension reform.

Some might interpret Righeimer's comments as more political rhetoric. They might be right. After all, if a guy's going to run for higher office he needs a plank in his campaign platform that is broader than little old Costa Mesa. His pal and OCGOP honcho Scott Baugh has stated that our city is "Ground Zero" for state-wide pension reform.A GREAT SITE

The pension numbers make my head hurt, but Communication Director Bill Lobell and Young have put together a site where you can find every answer to every question you might have about Costa Mesa pensions, HERE. It also includes a link, HERE, to a letter Young sent to the council in December that capsulizes much of that good information. The chart below is taken from that letter. (click on image to enlarge)

Labels: Bill Lobdell, Bobby Young, Jim Righeimer, Pension Reform, Scott Baugh

posted by The Pot Stirrer at 3/05/2013 02:56:00 PM

![]()

![]()

4 Comments:

Then there is recent article:

Study: Pensions could be credit problem for cities

One of the nation's leading credit-rating institutions, Moody's Investors Service, may soon begin holding California's state and local governments responsible for an estimated $328.6 billion in long-term pension debt – nearly triple the official estimate – if changes in the way Moody's independently evaluates credit are adopted as it proposed in July, according to a study by the nonprofit California Public Policy Center.

A key revision in Moody's proposal is using a market bond rate – about 5.5 percent in 2010 and 2011 – in place of an assumed rate of return on the investments that feed public pension plans. Many public pension systems, including the California Public Employees' Retirement System, or CalPERS, assume a rate of return on investments.

The adjusted unfunded liability figure under this new accounting breaks down to $8,600 per California resident, according to the study, which was based on data from the state controller's office. State and local public pensions would be 64 percent funded, compared with an official estimate by the state controller's office of 82 percent.

http://www.ocregister.com/news/pension-498199-public-moody.html

Luckily, the OC Register never slants one way or the other, and I know - I used to work there.

The OC Register is completely fair and never, ever tries to stir people one way or the other. They also love public employees with all their heart.

The OCR is so far left, it was Hugo Chavez's favorite newspaper. It's so progressive and liberal that it makes Gustavo and The OC Weekly look like Fox News..

Post a Comment

<< Home